Types of Loans and How They Can Help You Reach Your Goals

June 23, 2022

4 min read

4 min read

Use our online help center

so you can find your answers and

get back to what matters most

to you.

As the operator of a small business, you already know how important funding and cash flow are to your business’s trajectory. But are you aware of the types of loans that are available to you and what each type can help you to accomplish?

Maybe your business is long established and you employ a workforce, maybe you are starting out but primed for growth, or maybe you are just looking for capital to meet your day-to-day expenses. At whatever stage of your business’s maturity, the strategic use of debt is an important consideration as you think about its future growth.

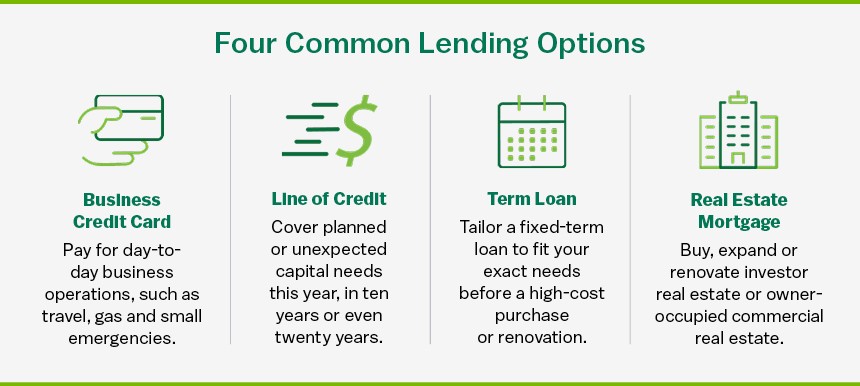

The best place to start is with the basics. There are many types of loans available, but the four most common are:

Each of these options has variables, and deciding which might be right for your business can take time. Knowing your specific needs will help you to determine what lending option or options will be best, as will talking with a relationship manager at your lending institution.

You are no doubt familiar with credit cards. Business credit cards operate much like the personal cards you’re used to. Business credit cards provide you with purchasing power, and are best used to pay for your day-to-day business operations—travel, gas, small emergencies and the like. Think about it like this: credit cards are for small purchases.

What does it take to open a business credit card? They are unsecured, meaning that you won’t need to put up collateral. Because of this, and because they help you meet your day-to-day needs, credit cards are often the most entry-level line of credit for a business.

Like a personal credit card, many business credit cards also offer rewards, such as cash back, travel rewards or points. They also usually have chip technology and self-service online account access. Most financial institutions, including M&T Bank, can brand the cards with your business logo or other design elements.

Think of a line of credit as your lifesaver. If you need to manage fluctuations in your business’s cash flow, opening a line of credit can quickly give you access to funds when you need them.

Businesses that open lines of credit have ongoing access to capital because, in most cases, once a line of credit is opened, it stays open—there is no fixed term. Say you need cash to pay your staff, or you need to buy additional inventory or pay a surprise bill that lands in your inbox. A line of credit will be ready for you whenever you need to use it, and will usually be accessible 24/7 via checks, ATM, telephone or in person.

Lines of credit backed by a guaranty from the U.S. Small Business Administration, or SBA, may have different terms, including a specific repayment schedule.

So if you have planned working capital needs or you encounter unexpected ones, having an open line of credit could cover costs this year, in ten years or even twenty years. Since lines of credit are not closed at the end of a term, they will respond to market rate fluctuations and will have variable interest rates.

At some point, your business may need to make a large purchase, such as buying a vehicle or renovating or improving your office space. If you have a high-cost purchase, a term loan might be the right route.

Your business may also have unique purchasing needs, such as, for example, aircrafts, construction vehicles or IT equipment. A term loan can be specifically designed for equipment financing like this. To ensure you get the best terms, you’ll want to look at the item you are financing and every possible way it could be financed, including terms loans, conditional sales, various lease methods and more.

Term loans can be tailored to fit your business’s exact purchasing needs, so they are a flexible loan option, offering a variety of amounts, interest rates and terms. They are mostly used to pay for tangible items that will be useful to your business operations.

These loans can be either unsecured or secured by collateral, largely depending on the size of the loan and your business and personal documents. They can also be variable or fixed rate. Because the details will need to be ironed out, you should plan on talking with a relationship manager at your lending institution.

When it comes to business lending for real estate, there are two main categories of loans: owner-occupied commercial real estate or investor real estate. The terms of each will differ.

Real estate loans are typically secured by the real estate itself. And they can be used beyond an initial purchase as well, for when you want to expand or refinance an existing property. You may even want to use one to build a new location.

When it comes to real estate lending, interest rates could be fixed or variable. The term length will vary depending on the type of property and the use.

Most lending institutions offer business banking clients access to a relationship manager to assist with services such as business lending. Talk to your bank to ensure you are making the most of your business lending options.

This content is for informational purposes only. It is not designed or intended to provide financial, tax, legal, investment, accounting, or other professional advice since such advice always requires consideration of individual circumstances. Please consult with the professionals of your choice to discuss your situation.

You are leaving our site

Please note that:

Such Third-Party Website's owner/operator may be regulated by governmental entities and laws that are different than those that regulate M&T.

Equal Housing Lender. Member FDIC. Bank NMLS #381076. ©2023 M&T Bank. All rights reserved.

Stay Informed

Subscribe

Get our newsletter for updates on today’s latest issues impacting business owners, including insider reports & special offers.

Want to learn more about other topics we haven’t covered? Tell us what interests you.

We cannot respond to customer service inquiries on this page. For assistance with your accounts or questions about M&T’s financial solutions, please call 1.800-724-2440.